Again this year, the Acimall Studies Office has published the statistics of the industry’s most significant companies. A traditional overview much appreciated by our readers.

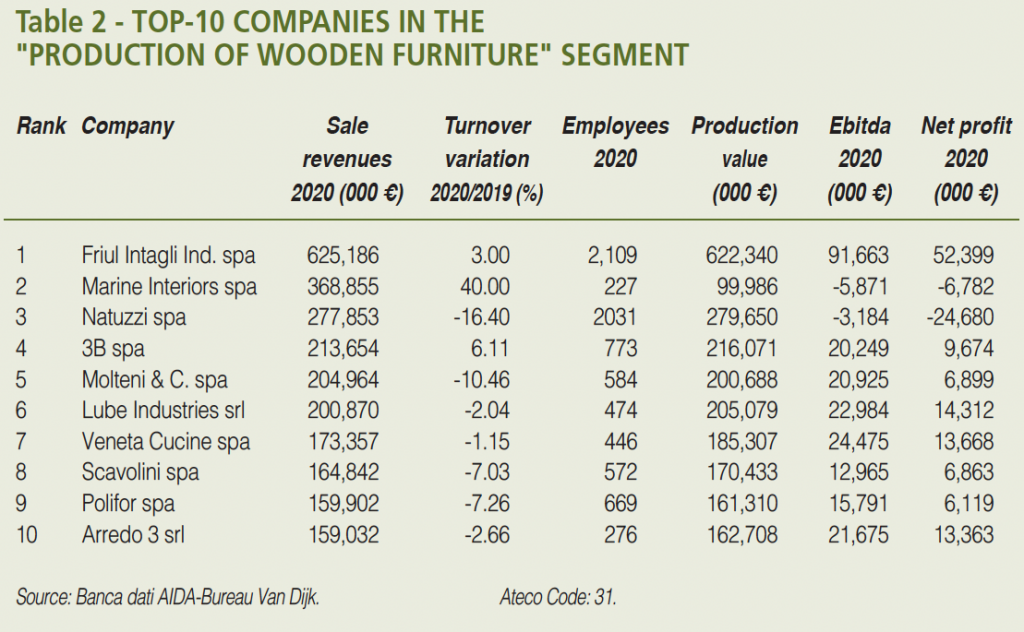

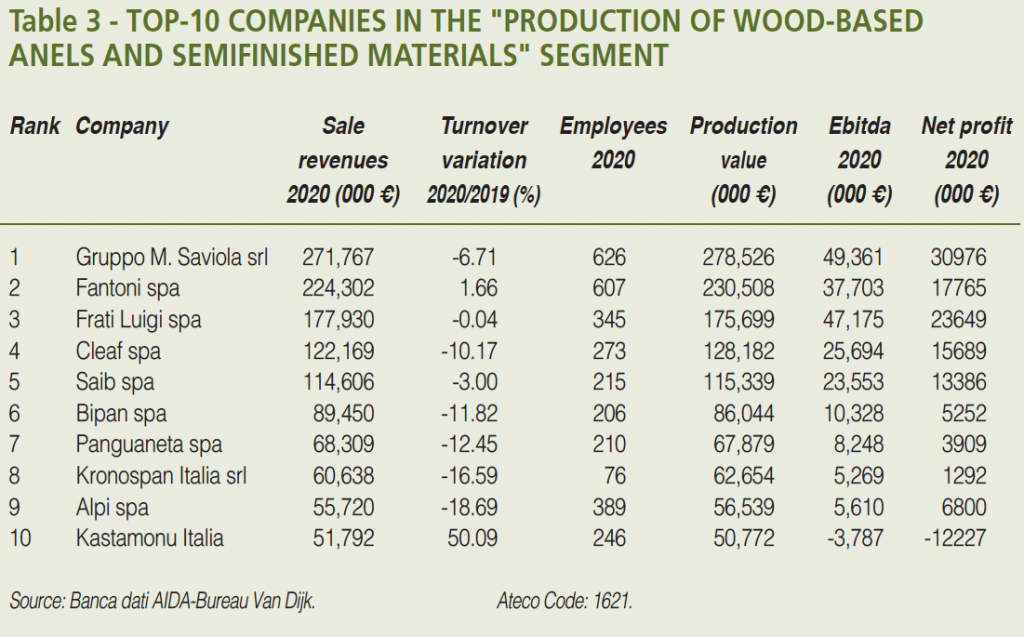

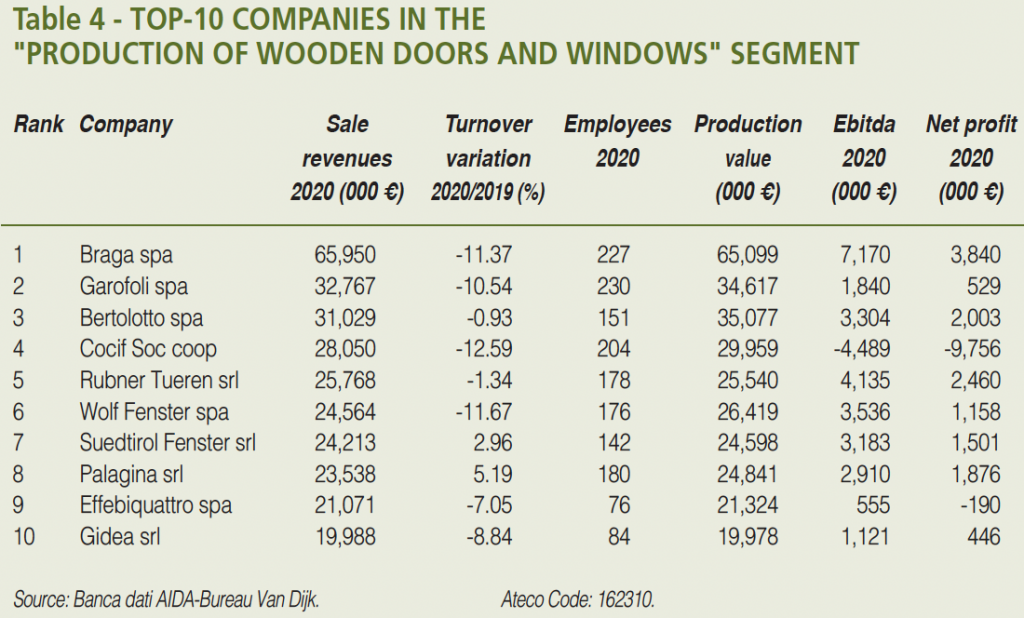

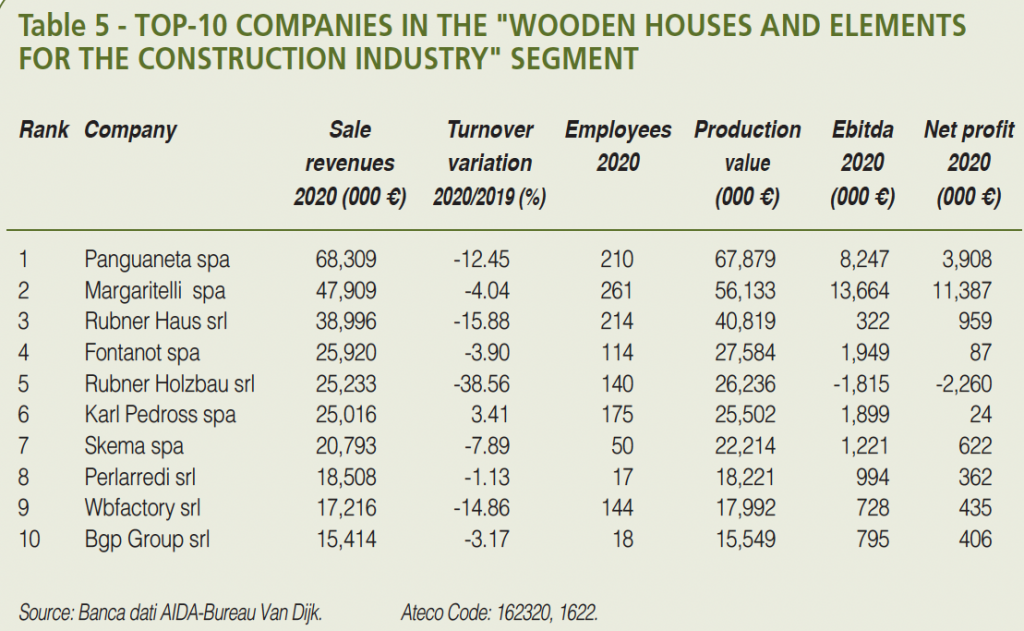

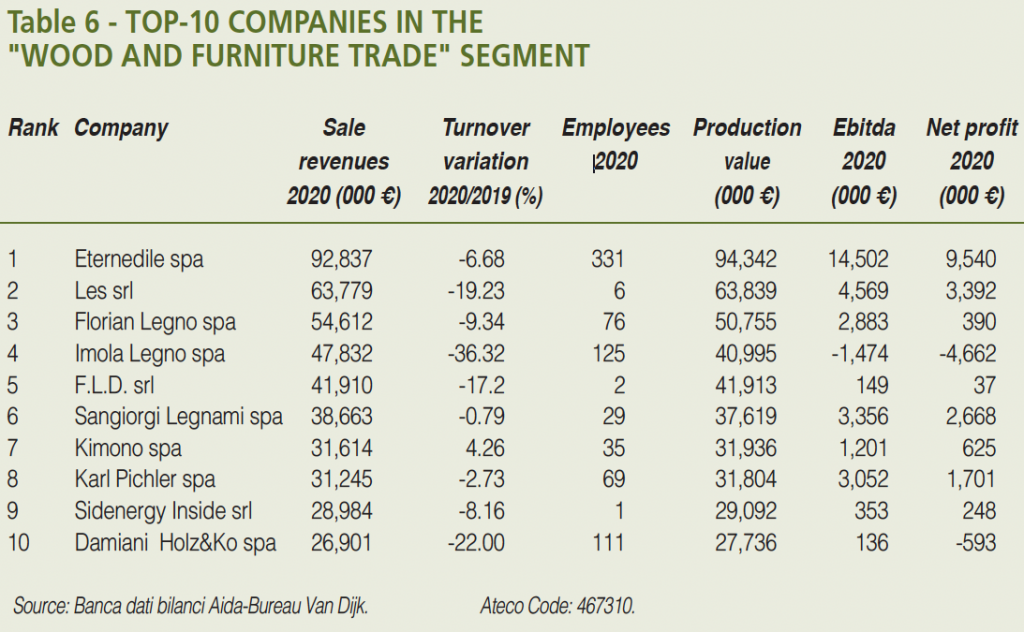

For Xylon, the Acimall Studies Office has laid down the ranking of the business results of wood-related industries, including “Woodworking machinery and tools”, “Production of wooden furniture”, “Production of wood-based panels and semifinished materials”, “Production of wooden doors and windows”, “Wooden houses and elements for the construction industry” and “Wood and furniture trade”.

The year under scrutiny is 2020, when companies had to “close down” due to the “Covid-19” pandemic. As you can imagine, this event had a massive impact on results.

WOODWORKING TECHNOLOGY

As usual, while offering an overview of the most significant wood-furniture industry segments, we are focusing on “our” industry, namely the sector of woodworking technology, showing figures that highlight the main trends in 2020.

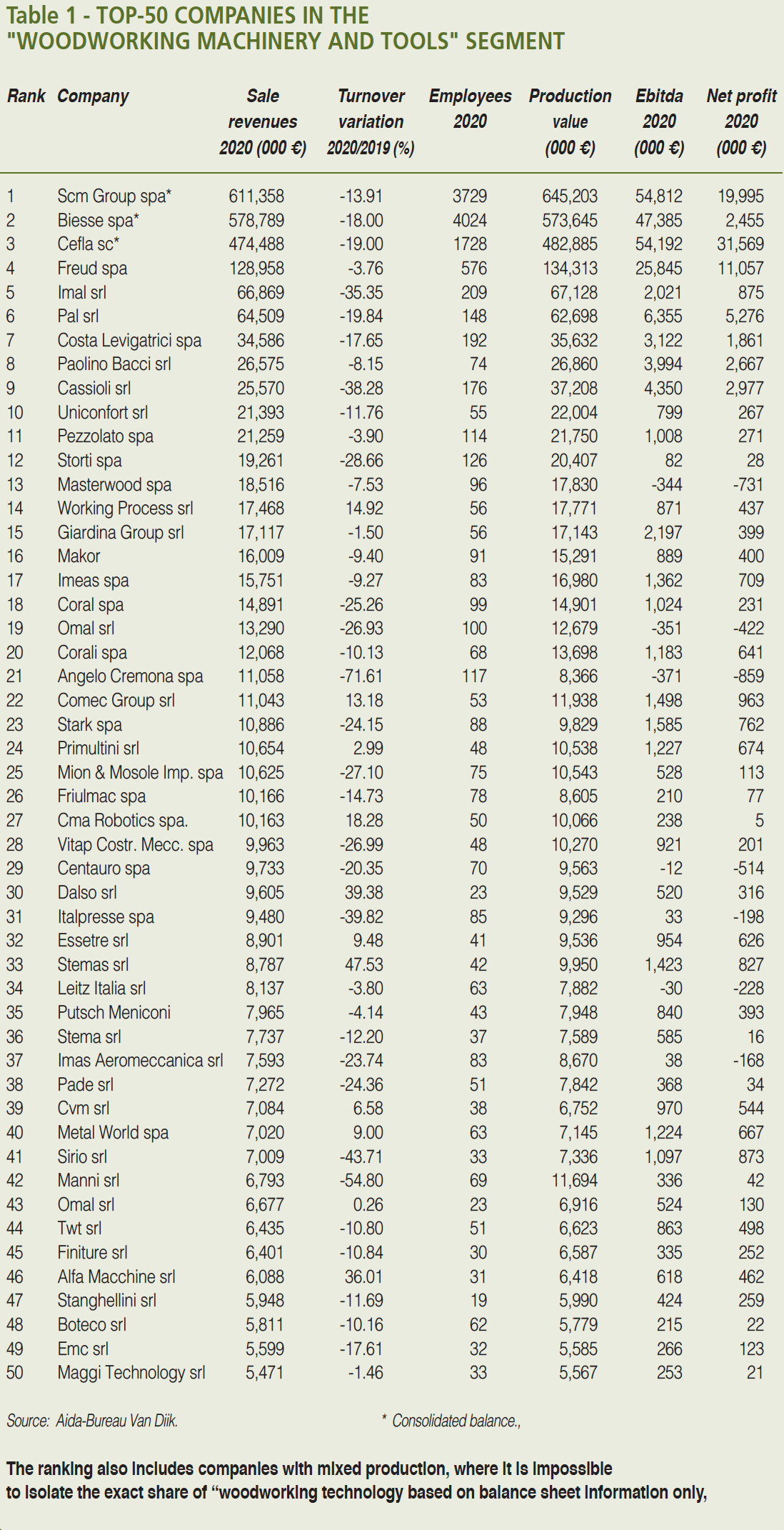

The analysis – summed up in the table – takes into account the top-50 Italian companies by sales revenues in 2020. Due to the lack of an Ateco 2007 code precisely identifying the activity of companies, the companies to be included in the ranking were selected by the Acimall Studies Office.

The ranking also includes companies with mixed production, where it is impossible to isolate the exact share of “woodworking technology” based on balance sheet information only.

Scm Group from Rimini, Biesse from Pesaro, and Cefla from Imola take the top-three positions. For the sake of correct information, we point out that the third-ranked company’s core business is not woodworking technology.

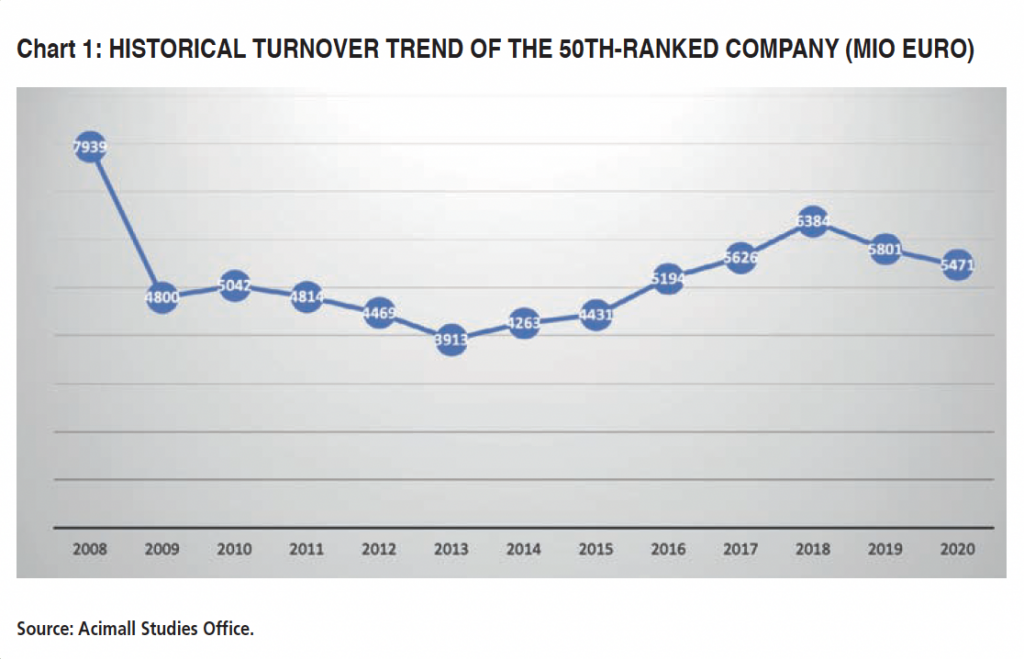

The 50 companies listed in the ranking have total revenues of 2,440 million euro, versus 2,953 in 2019, with an average value of 48 million per company (it was 59 in 2019). As you can see in chart 1, the revenue level of the 50th company, i.e. the first one above the “entry level” of our ranking, has decreased.

This is an inevitable consequence of the market conditions that characterized 2020 throughout.

Also notice that industrial activity restarted with a boost immediately after the lockdown, helping companies minimize the damage during the same year. The median, corresponding to the 25th position of the ranking (10.6 million Euro), is higher than the previous year, while the average Ebitda decreased, down to 4.5 million euro.

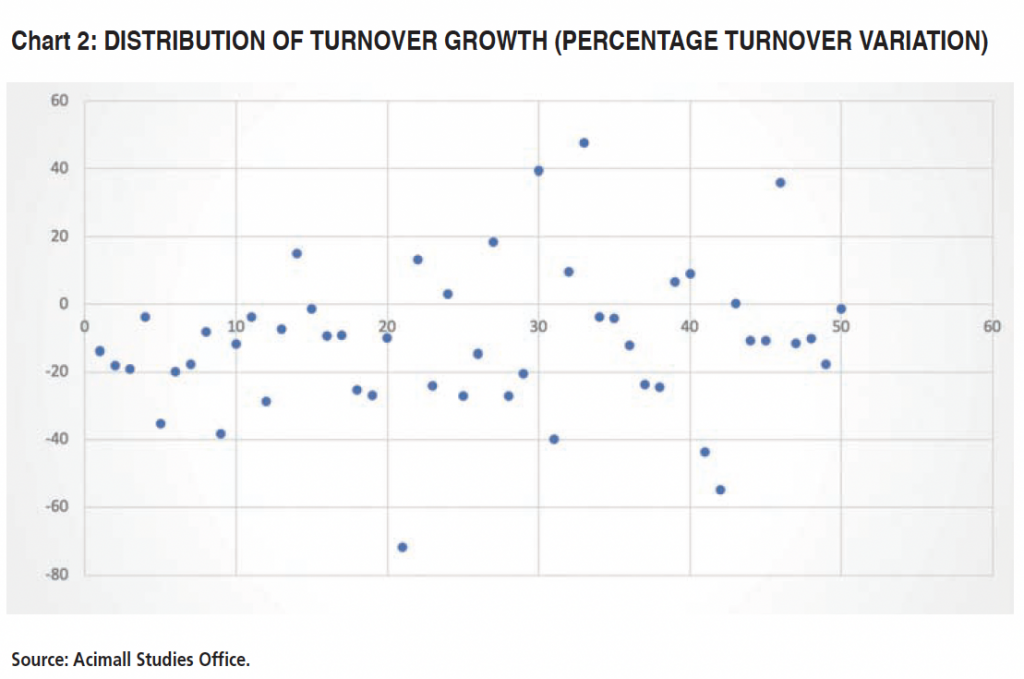

Chart 2 shows a large number of companies recording lower revenue levels, with heavy reduction in some cases, and few exceptions of companies reacting stronger than others when business restarted.

PAST, PRESENT AND FUTURE

Commenting upon these figures is really complicated, as business activity in the past two years has been heavily impacted by multiple variables. Starting from the events of the year under scrutiny, we must remember that, even before the “Covid-19” outburst, the global economy was already “creaking”, with the crisis of the automotive industry and the increase of international trade tariffs.

The forced lockdown in 2020 brought many companies to their knees, but recovery helped them partially make up for the suffered losses in the woodworking technology sector.

So, the year 2021 opened a new season with many positive signals and growing demand driving the production of technology for international and domestic markets, also supported by the energy efficiency bonus introduced in Italy for households, refunding 110 percent of renovation expenses.

2021 was an (almost) unprecedented year, also in terms of order growth rates; this economic phase also combined with a number of “exogen” factors that are forcing and will force companies to reorganize.

One of these factors is raw material shortage, which started to loom in early 2021 from the Far East and has extended shipping deadlines up to one year, combined with a disproportionate increase in shipping prices. To have an exact measure of price increases, just think that in 2020, shipping a 20-foot container from China to Italy cost 1,000 dollar approximately, while now it’s eight times as much.

Besides shortages, we are also seeing strong price increases that are forcing companies to bear surging costs to replenish their stocks that, as mentioned, must handle longer rotation cycles to the extended delivery times.

In this context, analyzing the current economic trend based on the increase in revenues or orders is definitely inappropriate. Increasing revenues without increasing margins must ring an alarm bell for the companies that, right now, are bearing higher costs for ordinary business.

It is also clear that we cannot ignore the situation in Russia and Ukraine, an event that must be taken into consideration when we analyze the situation of the woodworking technology industry. Ukraine, and most of all Russia, have always been key destination markets for Italian export, and in the short term, the trade flows to these countries will collapse.

In this uncertain picture, the Italian industry is maintaining its stability and has repeatedly demonstrated its ability to adapt to new situations and turn challenges into opportunities. Once again, the Italian industry is facing a new challenge, but past experience feeds hope for a positive outcome.

THE METHOD

The figures used in the rankings are taken from the Aida-Bureau Van Dijk database, which includes all the budgetary data of Italian companies.

The production activity of companies has been identified from to the corresponding Ateco 2007 code. Some companies have been included in a different business category, other than the activity specified in the balance sheet, based on patent and objective observation. We have also considered non-consolidated balance figures, with the exception of companies marked with an asterisk.

The calculation criteria are the following: Turnover variation: it is the percent variation of sales revenues compared to the previous year. Ebitda: it is a revenue margin that defines the earnings of a company before interest, taxes, depreciation, extraordinary components and amortization. Net profits: in the official balance sheet of a company, this value indicates the income of a company, net of costs and taxes. Production value: it is the sum of net revenues, stock-in-trade variations and other entries.