The American hardwood industry is navigating a period of uncertainty, marked by a significant decline in both high-quality and industrial-grade wood production. Output has dropped from 16.88 million cubic meters in 2022 to less than 12 million in 2024, a historic low. With weakening domestic demand for high-grade hardwood and a shrinking production landscape, international markets and sustainable forest management are becoming increasingly critical.

“The U.S. hardwood industry stands at a crossroads: while production declines, international demand, particularly from Europe and China, continues to evolve,” said David Venables, European director of Ahec (American Hardwood Export Council), the leading organization representing the U.S. hardwood industry in export markets. “Challenges related to tariffs, sustainability demands, and the EU Deforestation Regulation (Eudr) require new strategies to ensure a prosperous future for an industry largely composed of small landowners and family-run sawmills managing forests across generations.

We are at a crucial moment where environmental awareness is driving demand for sustainable materials. However, global competition and cost-cutting pressures often lead to economic compromises that risk undermining sustainability efforts. To navigate this landscape, we must embrace an intelligent selection of species based on their natural abundance and develop markets for all industrial grades, including traditionally underutilized species. By strategically utilizing different grades of both hardwood and softwood for specific applications, we can unlock the potential of the vast, underutilized U.S. hardwood fiber resource to meet global performance, cost-efficiency, and sustainability objectives”.

European market overview

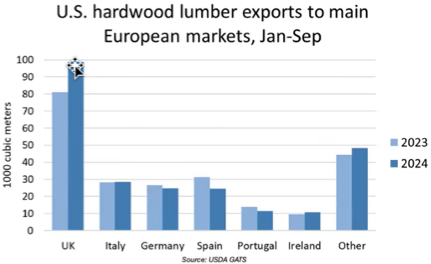

In recent years, European demand for American hardwood has shifted significantly. The UK, Germany, Spain, and Italy remain the top importers, with the UK registering a notable increase despite economic difficulties.

“This market is not dominated by large industries,” Venables noted. “Instead, it consists of many high-quality workshops—boutique, high-end facilities producing bespoke furniture for stores, restaurants, public buildings, and private residences. Spain and Italy also have a strong presence of small workshops, but much of our hardwood supply in these countries goes to industry, while in Germany, it is primarily used for engineered components, windows, and other specialized applications.”

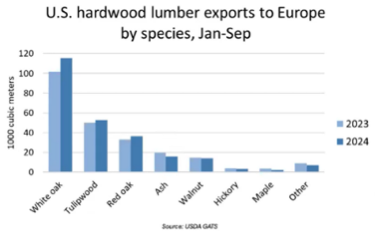

Regarding species preference, white oak remains the most in-demand, followed by tulipwood and red oak. “As shown in the chart,” Venables added, “cherry doesn’t even appear on the list, nor does maple, despite both being abundant in American forests. There is still much work to be done in educating architects, designers, and consumers about the incredible performance and aesthetic qualities of these underutilized species”.

China’s influence: tariffs, trends, and new market dynamics

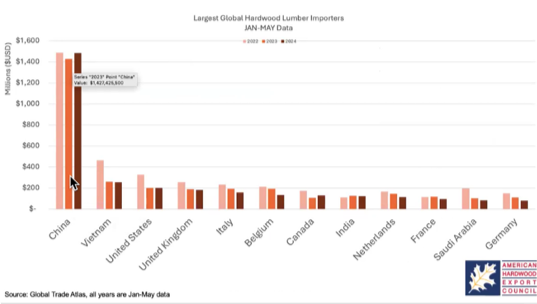

China remains the largest global importer of American hardwood, with volumes three to four times greater than secondary markets.

In value terms, China accounts for 44% of all U.S. hardwood exports, followed by Canada and Mexico (22%), Vietnam (10%), and Europe at 9%, with the UK alone representing 3%. However, shifting political and economic conditions are expected to impact future demand.

Following the imposition of high tariffs during the recent trade war, which significantly reduced demand, the Chinese market is now undergoing a major transformation. Imports of logs have risen sharply compared to processed lumber, signaling a new historic trend. This shift reflects China’s strategy to maximize its domestic sawmilling capacity. If Donald Trump returns to office and reinstates punitive tariffs, triggering another trade war, the American hardwood industry could face renewed challenges.

The uncertainty of Eudr: industry impacts

The European Union’s Deforestation Regulation (Eudr) presents both an opportunity and a significant challenge for the American hardwood industry. While the law’s implementation has been formally delayed until January 2026, debates over proposed modifications continue. This new approach to traceability and sustainability is set to reshape global trade dynamics and drive a new certification framework for forestry products.

“To ensure Eudr compliance and support global trade for the U.S. hardwood industry,” Venables concluded, “we are developing a highly sophisticated platform, the Sustainable Hardwood Coalition, where exporting companies can input shipment data, specifying the sourcing districts within each hardwood-producing state. Once operational, this platform is expected not only to address Eudr requirements but also to evolve into an independent global certification standard.

While we will not be fully compliant with the regulation at this stage—due to the vast number of forest landowners, we cannot provide geolocation data for every individual plot—we believe our jurisdictional, district-based system, while not meeting the letter of the law, will uphold its legal principles. In the coming months, we will seek a legal assessment on this matter.

Eudr has given us the opportunity to create something new, a global mechanism for real-time analysis and monitoring to demonstrate that forests are not being deforested. This is a tremendous opportunity to promote responsible forest resource management practices”.

by Ahec