We receive and publish the full version of the report produced by 24ORE Ricerche e studi and Mediobanca Studies Area on the health of the wood-furniture-lighting sector.

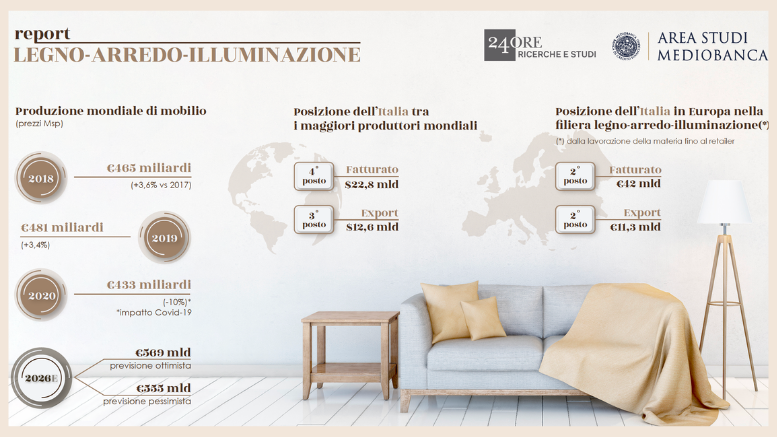

The world production of domestic and professional furniture (wood-furniture-lighting) is estimated at 481 billion euros. Italy shares with Germany the position of fourth world producer with sales of 22.8 billion, preceded by China, the USA and India. Also worldwide, Italy is the third largest exporter in the world of furniture and lighting, with a market share of 6.2 percent behind China (36.4 percent) and Germany (7.5 percent).

Adding up all the links in the wood-furniture-lighting supply chain (from the processing of the raw material to the retailer who sells to the consumer), the ranking of the five major European producers sees Germany in the lead with 73.8 billion euros, ahead of the Italy which follows with 42 billion and which in turn precedes France at 33.5 billion. Italy occupies the second position in Europe for the volume of exports of furniture and lighting, with a share of 16.5 percent (11.3 billion euros) of the total exported by the Union (68.4 billion), preceded by Germany with 19 percent, equal to about 13 billion euros, and ahead of Poland with 15.7 percent, equal to 10.7 billion. Italy is the leading European exporter to non-EU countries with 27.9 percent of the total, ahead of Germany at 21.5 percent.

These are some of the numbers in the WOOD-FURNITURE-LIGHTING Report prepared by 24 ORE Ricerche e Studi, the 24 ORE Group area that carries out complete and detailed analyzes of individual market sectors, in collaboration with Mediobanca’s Studies Area.

Even in a moment of global uncertainty, the Report provides the first hypotheses on the possible impacts and consequences of Covid-19, with the expectations for the current year in relation to turnover, exports and investments. The study, of over 300 pages, focuses on the financial statements of the last 5 years of listed and unlisted companies: data and tables are commented by the analysts of Mediobanca’s Research Area and integrated by a qualitative part created by Sole 24 Ore thanks to a comparison with some of the leading players in the sector. A sector Outlook is also proposed, created by Strategic Management Partners, accompanied by a Ceo’s Agenda. The report, which starts from a concise vision of business worldwide, identifying the major producing countries, frames the role of Italian companies on international markets and analyzes their performance. Particular attention is paid to issues such as import / export, governance, M&A operations, relocations, commercial dynamics and creditworthiness. The main valuation parameters are also examined: marginality, generation or destruction of value, return on capital, investments, productivity, labor costs.

Report WOOD-FURNITURE-LIGHTING

In the lighting and furniture production segments, Italy has 428 Italian companies with turnover exceeding 10 million euros, which have developed sales of 18.6 billion euros, employing over 72.5 thousand employees. In terms of size, medium-sized companies with Italian control prevail with sales of 7.3 billion (39.1 percent) and medium-large ones, again under Italian control, which invoice a further 7.4 billion (39.8 percent). ). The productions referable to the ‘high range’ achieved sales of 3.8 billion (20.4 percent of the total). Small businesses under Italian control account for 2.7 billion in sales, equal to 14.6 per cent of the total.

The 2018 turnover confirms the five best Italian players: Saviola Holding which operates in the wood and derivatives sector for 606.8 million euros, Inca Properties (Friul Intagli) which produces other domestic furniture for 591.1 million euros, Natuzzi in the armchairs sector and sofas at 428.5 million euros, Molteni – whose main business sector is living & sleeping – at 334.3 million euros and finally Fantoni (Novolegno), a wood and derivatives company at 331.2 million euros .

In terms of specialization, the processing of the raw product and the production of semi-finished products cuba sales of 3.9 billion. Among the finished furniture productions, the most representative is the one that includes chairs, tables and accessories with 3.7 billion. Contractors follow with 2.8 billion, lighting manufacturers with 2.1 billion and kitchens and upholstery both at 2 billion. The total of living room and night products, including bedrooms for teenagers, is just below with 1.9 billion, while the turnover attributable to pure bathroom furniture manufacturers is limited to 256 million.

A look to the future

Assuming that worldwide the wood-furniture-lighting supply chain undergoes a contraction of 10 percent in 2020, it would settle on a turnover of approximately 430 billion euros, roughly the size of the sector at the turn of the two-year period 2015-2016. The subsequent recovery in 2021 and the realignment to long-term rates for the following years would bring turnover to 485 billion in 2022 (roughly the level of 2019) and to 555 billion in 2026, almost sixty billion below the level expected before the pandemic. In a less pessimistic scenario, with a fall in world furniture production in 2020 in the order of 5 percent, the terminal value in 2026 would be around 570 billion euros, 15 billion above the worst case, but still 40 billion below the expected level before Covid-19.

As regards the Italian scenario, for 2020 a reduction of the sector’s production of 9.4 per cent is expected, mainly influenced (for 60 per cent of the total) by the drop in exports. To drive the relaunch, the companies in the sector have put in place a series of initiatives related to innovation, environmental sustainability, renewal of the corporate image and plans to tackle new markets and sectors. With the right tools and with the right priorities, the wood-furniture-lighting industry will be able to overcome this crisis as well, confirming its international competitiveness. The market recovery forecasts for 2021 could in fact be driven by foreign sales and reach a +5.3 percent.